By Kevin Flynn, from Seeking Alpha

The trouble with most Fed commentary is that so much of it tends to be rooted in the writer’s beliefs of how the world ought to work. I am often reminded of the 1980s thriller “Gorky Park”, whose inspector-protagonist Renko had a colleague (Pasha) with a singular knack for being able to redact any event into a triumphant expression of Soviet-Bolshevik party dogma, a cynical habit bred from the peculiar Soviet world that valued shows of allegiance over all else. I am often reminded of comrade Pasha when I read some piece forcing a number of useful observations into a similarly triumphant – and equally disjointed – dogma.

In recent weeks, the ongoing group of Fed policy dissidents has gotten new life and a fresh batch of recruits from the headline volatility around the now-infamous tapering discussion. A lot of angry dissidents with burnt positions from the near-universal sell-off in asset prices – especially concentrated in yield products and gold, as equities have obviously recovered – have been delivering withering conclusions about the Fed in the last few weeks.

Yet while there is no shortage of these thundering sermons being delivered from the mounts of gold, monetarism, emerging market assets, leveraged trading, and assorted abolitionists of central banks and governments in general, there hasn’t been much fresh insight. Most of it seems to be bent on either grinding the same old axe, or assigning blame for one’s trading losses.

For example, a couple of the more widely accepted nuggets of wisdom making the rounds is that one, the Fed butchered the job of communicating its policy intentions; two, the bank has become so frightened of the markets that it’s now their prisoner.

I’m not so sure about either point of view. One rough version of the taper story has it that Bernanke ineptly blurted out the bank’s intentions to taper, then had to send his governors running around to make up for the damage — so horribly feckless, the Fed.

But is that right? The reality is that there wasn’t, and never will be, an easy way to wean the trading herd off its addiction to the milk of easy money. What’s more, the herd is never able to change course easily, regardless of what the prevailing narrative or folklore is for buying or selling something. Hyman Minsky (I just discovered) posited something I’ve been writing about lately, namely that stability breeds instability (his words), a clever phrasing that I had been using many more words to express. It comes to the same thing – the longer some trend appears to be safely in place, the more traders will resort to leverage and speculation to profit from it, thereby making any change at all problematic.

But looked at from an elevation of ten or twenty thousand feet, it appears that the Fed has gotten very close to exactly what it wanted, at least insofar as being able to introduce the possibility of tapering without unhinging the markets. So what if the governors fanned out post-meeting to smooth the message – when you think about it, anyone with half a brain could have predicted it (I know, because I did predict it). Equities have recovered to new highs, and bonds and other assets have shaken off some of the damage. Leveraged trades have gotten a very useful lesson in not hanging the head out of the window.

It seems to me that it’s the markets that are mishandling the communications work. In their eagerness to justify stock prices, for example, or record amounts of bond inflows, asset managers haven’t challenged certain assumptions, like why long-term Fed outlooks haven’t come true since the crash. Like other central banks and monetary authorities, the Fed is constrained from saying certain things publicly, whatever their members may privately believe.

The most glaring contradiction has been between the warmly eager embrace of quantitative easing, at least as expressed in asset prices, with the fact that most of the senior investment world has been perfectly content to slip past the inconvenient truth that the Fed wouldn’t be doing any of it if it was really confident about the economy. In particular, it would not be preaching zero interest rates for two more years.

One of the reasons I like the Pimco duo of Bill Gross and Mohammed El-Erian is their emphasis on the economy and practical considerations, rather than dogmatic screeds about gold, monetarism or creeping (fill in the blank). They are still buying bonds on the premise that the economy is as anemic as the actual data and actual Fed policy says it is, rather than basing investment policy on the institutionally biased junk-pile of Wall Street earnings forecasts, Fed long-range outlooks, and rosy-eyed fawning from the business media.

I would like to see a better discussion (without the usual polemics) about two issues that appear to be joined together at the hip – one, why the Fed should want to be tapering early while promising two more years of zero interest rates, and two, what might the Fed’s policy response be in response to trouble from overseas – in particular, Europe and China.

In support of ZIRP and Messrs. Gross and El-Erian this week is once again the latest round of data. The latest round of retail sales data show that year-on-year sales growth for the second quarter fell to 4.13% – the lowest second-quarter rate since 2009. The sales rate ran 3.7% higher through the first six months of 2013, 3% excluding gas and autos, not much above the inflation rate and part of a steady decline. The ex-auto ex-gas sales figure actually fell 0.1% last month, and even a big revision back up to +0.2%, for example, would still leave spending on the downslope as we enter the long-ballyhooed second half, in which all things economic are said to recover, thereby justifying – finally – the long run-up in equity prices.

Housing starts industrial production data are two more good examples. Housing is still doing alright, but the year-on-year rate of starts growth has slipped to about 20% through the first six months from 27%-28% in the first quarter. More telling is industrial production data. Maybe the June “rebound” topped consensus, but the year-on-year rates in May and June were below 2% (1.6% and 1.8% respectively) for the first time since February of 2010.

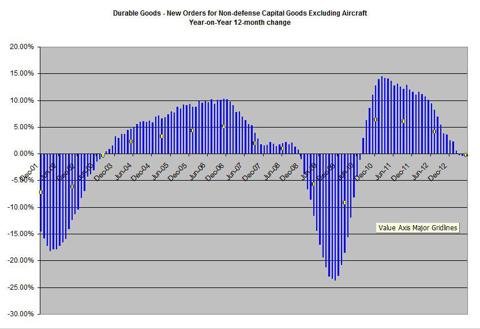

For illustrative purposes I’ll reproduce my chart on the year-on-year change in 12-month business investment spending:

The reason for doing so is a Bloomberg piece that ran over the weekend glowing about how the “surge” in corporate investment spending (!) – based specifically on the above data – is going to offset the sequester. You can’t make this stuff up.

Assuming then that the data, Bernanke, Pimco and possibly even myself are right about what the economy is actually doing, rather than what it might do if every tumbler drops correctly on the global economic lotto game, then the Fed may have good reason within its benighted world to be talking about keeping interest rates at zero for another couple of years. The real issue is why the Fed is talking about tapering at all (putting aside the response of belated recognition of its hopelessly unsound and doomed policies, because I don’t think that’s how the governors see it).

It’s one of the two joined-at-the-hip issues, and I invite SA readers to chime in with their thoughts. Two reasons that aren’t a stretch include the idea that the Fed doesn’t want any fresh, 2006/2007-style asset bubbles popping up, and the simple thought that the governors may indeed be worried about the effects of the huge balance sheet expansion.

A more speculative reason that I have hinted at is that despite the brave talk about having lots more policy tools, in truth the Fed isn’t currently well placed to handle another big financial crisis – and both the eurozone and China have been nearing the proverbial ditch of late. It might be far more effective in a crunch for our own bank to return policy accommodation to $85 billion/month, rather than having to raise it to $125 billion/month. It’s something worth thinking about, and something the Fed would not be anxious to talk about.

Time for a few predictions. One is that we will look back on the current obsession with Fed bond purchases as the ultimate guide to asset pricing as a major valuation mistake. A second is that the Fed does indeed start to taper this fall, not because unemployment is headed below 7%, but because of the worry it’s going to need some slack in the rope if things start to fall apart abroad.

Finally, the current rally will soon run out of steam. It may run out today, when Bernanke goes to the Senate and perhaps confesses to his evil plan for taper intentions, or it might wait until the end of next week, when the second quarter earnings momentum traditionally fades. In either case, it’s time to start working on your list of things to sell.